Yeah, I agree. We should align the LTV and liquidation threshold with those of earnAUSD. For now, a 10M cap is probably the best option, and we can increase it later if the supply cap is reached.

Clarification on Asset Configuration, Risk Parameters, and Isolation Mode

I want to provide additional clarification on the asset configuration should this proposal pass, as this is the first time these topics are being discussed publicly. In the near future, I’ll publish a dedicated post standardizing these concepts so users can better understand the available options, associated risks, and operational framework before participating in discussions around new asset listings.

Neverland introduces new assets conservatively and expands risk parameters only after an asset has proven itself in production.

The initial configuration would likely look as follows (due to final risk review):

Initial Launch

| Loan-to-Value | Liq. Threshold | Liq. Penalty |

|---|---|---|

| 75% | 80% | 10% |

Maturity to Max

| Loan-to-Value | Liq. Threshold | Liq. Penalty |

|---|---|---|

| 85% | 90% | 5% |

For those unfamiliar with these parameters:

- Loan-to-Value (LTV) is the maximum amount users can borrow against supplied collateral.

- Liquidation Threshold (LT) is the point at which a position becomes eligible for liquidation.

- Liquidation Penalty (LP) is the discount liquidators receive when repaying unhealthy debt, incentivizing liquidations and protecting protocol solvency.

The timeline to reach the maximum configuration depends on several factors, including onchain liquidity, market depth, protocol protections, operational risk, and observed asset performance over time.

Similarly, the proposed supply cap should not be viewed as the launch cap. Rather, it represents the maximum cap that may eventually be reached once the asset has demonstrated sufficient maturity. A supply cap is the maximum amount of an asset that can be supplied to the protocol and serves as one of the primary mechanisms for limiting protocol exposure.

On Neverland, we intentionally avoid maintaining large unused headroom and instead keep supply caps close to actual utilization. As demand increases, caps can be expanded through the Risk Timelock process. This means that even in a worst-case scenario, the protocol’s maximum exposure is limited to the difference between the current supplied amount and the configured supply cap.

This has been a core risk management practice on Neverland since the early days of the protocol. Rather than provisioning excessive capacity upfront, we scale risk parameters based on demonstrated demand and observed market conditions. This approach is precisely why Neverland would not, and will not, face situations similar to the Aave rsETH incident, where excessive available capacity significantly increased protocol exposure. Risk parameters on Neverland are intentionally conservative at launch and expanded only when justified by liquidity, adoption, and market maturity.

Another important consideration is that Isolation Mode remains an available option for discussion during the risk review process and may be considered for the initial listing depending on the final assessment.

Isolation Mode is a security framework designed specifically for assets that require additional observation before receiving full collateral permissions. When an asset is listed in Isolation Mode, users can still supply it as collateral and borrow against it, but with important restrictions that significantly reduce systemic risk.

Specifically:

- The asset can be used as collateral.

- Users borrowing against the isolated collateral can only borrow assets approved by governance for isolation mode, which are

USDC,USDT0,AUSD. - A dedicated debt ceiling is enforced, limiting the total amount that can be borrowed across the entire protocol using that isolated asset as collateral.

- Users who choose to use an isolated asset as collateral cannot simultaneously use other collateral assets to increase borrowing power.

In practice, this means that if users supply in this case syzUSD as collateral, they would only be able to borrow approved stablecoins up to the isolation debt ceiling established by team as risk operators. This prevents risk from spreading throughout the broader lending market while still allowing the asset to be utilized productively within the protocol.

The debt ceiling and supply caps would grow progressively alongside liquidity, adoption, and confidence in the asset. As the asset demonstrates stability and operational resilience, the team can with a follow-up proposal can consider removing isolation restrictions and expanding collateral permissions to the rest of the markets.

This approach allows Neverland to gather real-world performance data while maintaining strict controls around protocol exposure. It is one of the most effective mechanisms available for introducing new collateral assets safely.

We take asset listings extremely seriously, and nothing on Neverland is introduced based on arbitrary assumptions. Risk parameters are intentionally conservative at launch because configurations can always be expanded as an asset matures. The opposite is far more difficult and disruptive for users, so it’s always safer to start conservative and increase the configurations.

In the coming days, I will also publish a security review from our team covering operational analysis, bridge architecture, backing mechanisms, administrative controls, smart contract security, and any outstanding questions for the Yuzu team, along with discussion points for the community to review and evaluate.

In the meantime, feel free to tag me with any questions regarding listings, risk management, or how Neverland’s lending system operates. Historically, asset listings were reviewed directly by the team, so many of these processes have not yet been explained publicly in detail.

6 Likes

I wasn’t a fan when Curvance added them, and feel the same or stronger about Neverland adding. I see and agree with what others have stated about the thoughtful strategies employed by Yuzu. My big fear with Yuzu is just that they seem so immature as a project. While researching them when Curvance added, I joined the DC and was struck by how few members it had. Maybe 200 or so? I couldn’t rejoin, the link on their site has expired and not been replaced. The Yuzu TG has 64 members though, and is announce only. So, if/when one of us needs help (or the next scare hits), will they have a robust set of support mechanisms? I’m not seeing it. Anyway, being new, or small, isn’t inherently bad. But I think a $120M protocol allowing a small, not-yet-battletested protocol in with a cap of $20M risks a massive contamination if something goes wrong. And, if we’ve learned anything in crypto, we know that ANYONE can get got. Would feel much better if you let them in via an isolated market. Let those comfortable with that type of non-bluechip risk shoulder it and reap the gains. My 0.02 ![]()

1 Like

Another question after researching this more – it appears syzUSD is native to Plasma (in terms of staking and unstaking). What bridge(s) support moving this token to/from Monad and what is the bridge risk involved? I apologize for my ignorance on this token, I’ve only heard about it for the first time since this RFC opened.

LayerZero OFT (3 DVN not 1) and discussion regarding migration to Chainlink CCIP

Third question – is there enough liquidity on Monad to handle liquidations of syzUSD in the event of a depeg/DeFi exploit elsewhere.

Liquidity is the secondary market, in a stressed scenario, liquidators have the option to bridge the asset back to Plasma, unstake it, and redeem at ~1:1 for the underlying yzUSD. This asynchronous redemption path significantly reduces liquidation risk compared to pure on-chain spot liquidity.

Why start with $20m supply cap?

Are you expecting this supply cap to be reached and in what timeframe?

We propose starting with a $20M supply cap to strike a good balance between giving the market meaningful room to grow while remaining prudent during the initial phase.

Given the yield-bearing nature of syzUSD, we expect users to actively engage in looping strategies (deposit syzUSD → borrow stables → buy more syzUSD). A relatively generous initial supply cap facilitates this flywheel and should help drive strong borrow demand for USDC, AUSD, and USDT on Neverland.

if Yuzu lost 20% of its backing tomorrow, what exact mechanism prevents Neverland from inheriting those losses?

The yzPP (Yuzu Protection Pool) , the junior first-loss tranche, absorbs losses first and entirely until it is depleted. Only after the yzPP is fully exhausted would any loss impact yzUSD/syzUSD holders.

Additionally, the protocol benefits from proactive safeguards including Hypernative Sentinel for real-time threat detection, Fordefi MPC for secure operations, and other internal tools + monitoring. These systems have proven highly effective in past incidents (notably with Fluid), where the team was able to react within the first second.

That said, no system can eliminate risk entirely, even the largest stablecoins like USDC or USDT can experience depegs. This structure, however, provides a strong layered defense that significantly mitigates downside for Neverland.

On this request, why doesn’t Yuzu Money have a size in mind for the DUST commitment and timeframe? Also, why isn’t Yuzu Money offering to match the commitment? This feels like a lack of plan or you’re expecting Neverland to fund your defi expansion. Which is unacceptable either way.

This has to be discussed in a second plan, a second proposal

I see and agree with what others have stated about the thoughtful strategies employed by Yuzu. My big fear with Yuzu is just that they seem so immature as a project. While researching them when Curvance added, I joined the DC and was struck by how few members it had. Maybe 200 or so? I couldn’t rejoin, the link on their site has expired and not been replaced. The Yuzu TG has 64 members though, and is announce only. So, if/when one of us needs help (or the next scare hits), will they have a robust set of support mechanisms?

Thank you for the honest feedback.

-

Telegram is announcement-only.

-

We’ll fix the expired Discord link right away (thanks for pointing it out).

Community size isn’t the best quality metric, we prefer focusing on code, audits (Pashov + Dedaub), execution, and product robustness. Yuzu has already been battle-tested in recent DeFi events (including rsETH, Fluid, etc.), where our systems reacted effectively within seconds.

We understand the “small protocol risk” concern, the final figures will be set by Neverland’s risk team.

Happy to provide more data if needed.

3 Likes

I’m sure I’m not fully understanding everything fully, but I’ll ask my dumb question anyway. Does Yuzu already use Neverland as part of its on-chain overcollateraiized lending strategy? Like is it already looping USDC/USDT/AUSD on Neverland under the hood? Maybe it’s no big deal if it is, but wondered if it was an additional risk cascade point of failure.

Anyway, I’ll keep trying to understand it better.

The answer to this should be NO, as Neverland is not whitelisted.

Maybe @TelosConsilium can confirm, but I don’t remember Neverland even being in the discussion.

P.S. If this proposal fails, Yuzu should at least get some decent publicity out of it, many people just have discovered them through it ![]()

No.

All strategies that back yzUSD are supported by the proof of solvency provided by Accountable: https://yuzu.accountable.capital/

No funds are held off-chain; everything is on-chain and verifiable even without Accountable.

Furthermore, as the previous comment pointed out, Yuzu Money has a protocol and asset whitelist system, and Neverland is not on it.

This system is designed so that you have at least one week before a change is implemented.

This allows anyone who is not aligned with a protocol/asset to withdraw before the change.

As we explained previously, Yuzu Money is concerned about its internal risk as well as its users

1 Like

True, only loaznd but you can’t lend more …

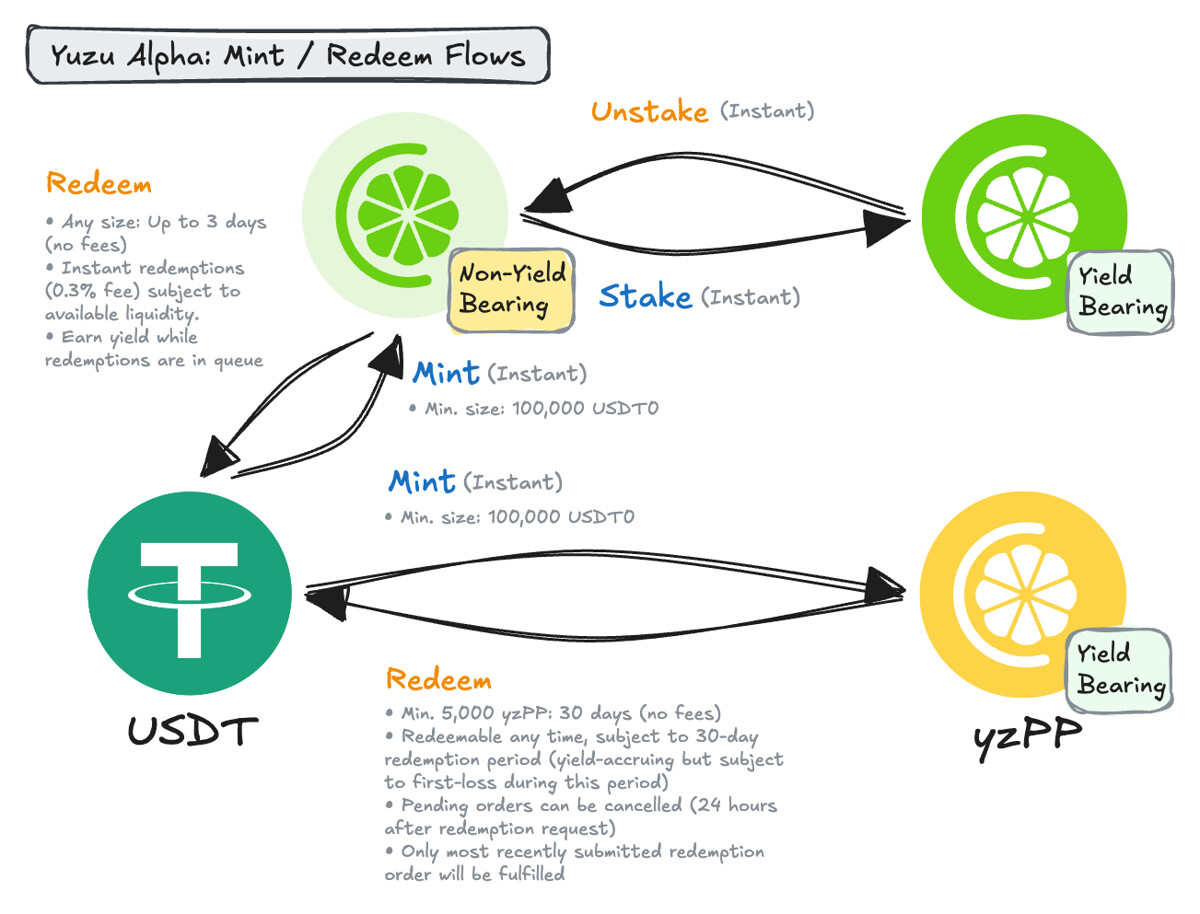

Minters mint/redeem yzUSD and yzPP with USDT0, subject to each related rule and prerequisite. Inflows are placed into the Collateral Pool and then deployed into curated DeFi strategies per policy. Flow diagrams (mint/redeem and protocol fund flows) are shown below.

![]() Access to primary mint/redeem flows for yzUSD and yzPP are limited to Eligible Investors who have passed KYC/KYB/AML, Sanctions, and Source‑of‑Funds/Wealth checks and who have provided reasonable proof of status plus a declaration to be treated as such. Secondary‑market activity in yzUSD/syzUSD is not operated by Yuzu and remains subject to third‑party venue rules and law.

Access to primary mint/redeem flows for yzUSD and yzPP are limited to Eligible Investors who have passed KYC/KYB/AML, Sanctions, and Source‑of‑Funds/Wealth checks and who have provided reasonable proof of status plus a declaration to be treated as such. Secondary‑market activity in yzUSD/syzUSD is not operated by Yuzu and remains subject to third‑party venue rules and law.

Documentation: Mint & Redeem | Yuzu Money

2 Likes

100k min is a high benchmark

I strongly advocate that this proposal have the LTV dropped to 85% and supply cap at the discretion of the Neverland team. $20M is, in my opinion, an insane risk with a pooled lending protocol. This is 2X the amount present on Monad.

I am also not a fan of “lets bridge this asset to Plamsa to liquidate it”. The blockspeed of Monad is its greatest asset. We need DEX liquidity on-chain, period. The Yuzu teams needs to incentivize more TVL in the existing Balancer V3 pool.

Without these changes to the proposal, I will be voting NO.

5 Likes

Liquidity is the secondary market, in a stressed scenario, liquidators have the option to bridge the asset back to Plasma, unstake it, and redeem at ~1:1 for the underlying yzUSD. This asynchronous redemption path significantly reduces liquidation risk compared to pure on-chain spot liquidity.

The more I think about this, the flows for liquidators seems really difficult if we have to depend on bridging. Bridge to Plasma, unstake to yzUSD, convert to USDT (not sure if USDC is supported), bridge back to Monad, pay off loan. Most loans will be AUSD and USDC.

In my mind, the liquidation flow is the most critical risk for Neverland and the limited DEX liquidity (or native support by Yuzu to unstake syzUSD directly to AUSD/USDC on Monad) is a very real problem.

Clearly it got listed on by a Morpho curator and by Curvance, but I don’t think we should use that as the benchmark for Neverland.

3 Likes

I agree that the bridging path adds complexity and potential friction for liquidators. However, having a reliable 1:1 redemption mechanism (independent of secondary market price) is, in our view, far more important and sustainable than trying to bootstrap deep DEX liquidity through perpetual incentives.

Incentives can never be provided infinitely; they eventually run out or become unsustainable, leaving the protocol exposed. A built-in redemption path back to yzUSD at ~1:1 gives liquidators a clear, trust-minimized exit that doesn’t rely on pool depth or market conditions. This significantly reduces liquidation risk for Neverland compared to pure spot liquidity.

1 Like

Virtually all of the supply is concentrated in about 6 wallets. Out of 664 total holders on Monad, 656 of them, all but 8, have less than $100 worth. This seems like a significant risk.

3 Likes

This is one of the greatest points, of all the great points, made by this community regarding this proposal. I’m probably the least versed on the nuances of this initiative, but it feels somewhat like Neverland, and Monad inherently, are being used by Yuzu as a satellite launching pad, while offering little to Neverland and/or Monad in return. Neverland and Monad will grow organically over time. I would personally like to see the growth come from healthy cohesive relationships with projects that deserve a seat at the table. This community is not desperate, and projects and opportunities will always present themselves.

3 Likes

Actually, it is more like Neverland is incentivizing that pool right now…

I agree on this part.

I’m just very skeptical of how the yield is earned and what risk parameters there are. I have seen other similar coins with baked in yield get paused for withdrawals because some of the pools they were using had issues. I do not have the time to do a full risk assessment, but that is certainly needed, and I feel the negatives of what it opens Neverland up to is not worth any potential benefits. I have seen less than 5 people personally ask for this as an asset. I have seen way more people asking for xAUT0 than this assist. Just my two sense.

1 Like

Having read through everything here (and being generally unfamiliar with the asset myself), I’d trust the team here on most everything and generally would be in favor of adding. However… the one thing that stands out as a potential issue is the supply cap of 20M. That’s pretty large compared to other current assets on Neverland including earnAUSD (as others have pointed out) and WETH. I’d be in favor of this proposal if the supply cap was reduced to 5-10M, with the ability to increase at a later date subject to performance.

2 Likes

Conversely… if there’s a reason why a 5-10M cap might be too limiting… would love to hear it!

Not sure I see a problem with this and would like the input and explanation of others. It’s only for collateral and can’t be borrowed. A cap would be appropriate but some lost boys may want to invest reciprocally. The holders are concentrated both on plasma and monad, but that’s common with new protocols. Seems like their yield is based on OK investments. It seems like they are just “packaging” other stables and defi. It takes $100k just to mint any of their tokens which means it’s not geared for pump and dump shrimps. I did throw them a benji for fun, and I know redeeming it requires cross chain mojo, but I that is what it is when you start on one chain and try to break into another. Neverland might see similar adoption resistance on another chain, it just happens monad is the new house on the block. Convince me not to vote yes. I feel Neverland mgmt wouldn’t even propose this if vetting and background research had not been already done.

1 Like